Enterprise Risk Management

Vichara leverages its expertise in risk management, financial modeling and big data management to provide highly transparent regulatory solutions.

Vichara, with its business domain and technology expertise, is uniquely placed to help financial firms comply with growing regulatory requirements. We assist our clients overcome quantitative and operational challenges to meet the demands of auditors and regulators for better transparency and increased due diligence

Vichara has special expertise in analyzing structured products such as RMBS, CMBS, CLOs, ABS CDOs, other consumer ABS as well as residential mortgages, commercial mortgages & corporate loan portfolios. Vichara utilizes its risk modeling framework powered by big data management & analysis platform to develop, validate and fine tune risk models using large scale historical data. The analytics framework integrates 3rd party & proprietary models and runs on a high performance distributed computing environment (grid/cloud) to analyze large portfolios in a short amount of time. Our solutions address requirements mandated by regulatory frameworks like Basel, Dodd-Frank and IFRS.

Stress Testing in the US: CCAR & DFAST

Stress Testing

Vichara helps financial institutions perform CCAR and DFAST stress tests to meet the Federal Reserve’s evaluation criteria for assessing their resilience to adverse market developments.

Vichara’s solutions support securitized products such as RMBS, CMBS, CLOs, ABS CDOs, other consumer ABS as well as their underlying collateral like residential mortgages, commercial mortgages & corporate loans. Risk measures like probability of default (PD), loss given default (LGD), exposure at default (EAD) are produced for assessing capital planning and capital adequacy. Customized reports for internal reporting as well as for submissions to regulators can be produced using our solutions.

Our experience in analyzing large portfolios at most granular level using highly parallelized computing framework enables us to perform these tests in a time efficient manner.

As part of Vichara’s solutions for stress testing, our clients analyze their portfolios under various stress scenarios while also having the ability to:

- Build new risk models or extend existing client models using Vichara’s modeling framework. Vichara’s modeling framework helps incorporate macroeconomic indicators and multiple data sources to develop an appropriate risk model.

- Integrate existing proprietary or 3rd party risk models.

- Create additional stress scenarios and analyze impact on portfolios.

- Combine large collateral data sets with model projections to analyze risk distribution.

Stress Testing in the UK & Europe: PRA & EBA Stress Tests

Stress Testing

For UK and EU financial institutions, Vichara provides solutions to perform stress tests as mandated by the Bank of England’s Prudential Regulation Authority (PRA) and the European Banking Authority (EBA). The tests are conducted using consistent methodologies, scenarios and key assumptions as mandated by respective regulatory authorities.

Vichara works closely with its clients to implement highly transparent, defendable and auditable solutions. Using our high performance and cost efficient solutions for loans and structured products, our clients can analyze large portfolios in short periods of time. Highly modular architecture allows us to integrate client’s proprietary credit models. Additionally, using Vichara’s modeling framework, clients can build new predictive credit models or extend and fine-tune existing models.

We help our clients formulate and execute stress analysis using scenario definitions provided by PRA or EBA. In addition, Vichara also helps clients analyze portfolio performance under additional scenarios as per client`s own macroeconomic views. Our solutions enable our clients to attribute performance to various risk factors. The solutions also provide high level of flexibility to integrate with client`s internal processes and meet future requirements from regulators.

Basel for the US: SSFA

Capital Adequacy

Vichara’s SSFA compliance solutions use risk weighted methodology for computing regulatory capital charges for securitized exposures as per Simplified Supervisory Formula Approach (SSFA). The solutions cover Agency and Non-Agency RMBS, CMBS, and consumer ABS.

Clients can analyze their portfolio of securitized assets to compute risk weights and capital charges for securitized assets compliant with SSFA methodology. We leverage our collateral mapping database at deal, group, tranche and loan-level to do the computations and also provide collateral mapping between different data sources giving clients the flexibility to choose their preferred data sources.

The RWA and capital charges are computed every month as new remittance data is available. Current as well as historical data is tracked within the solutions for comparison, time series analysis and reporting.

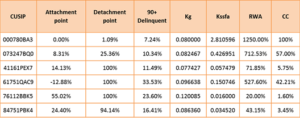

As an illustration below, Vichara’s solutions provide a breakdown of key components contributing to computation of capital charge:

- Weighted-average-risk-weighted capital requirement of the underlying exposures (Kg)

- SSFA ratio (Kssfa)

- Risk weighted assets (RWA)

- Capital charge (CC)

Basel II, 2.5 & III

Vichara’s high performance modeling framework coupled with the highly scalable analytics framework facilitates forward looking performance analysis on credit portfolios comprising of loans (residential mortgages, commercial mortgages, & corporate loans) and structured products (RMBS, CMBS, CLOs, ABS CDOs, SLABS, and other consumer ABS). Vichara’s modeling framework helps develop historical regression based models to predict future performance correlated to macro-economic factors.

Vichara solutions help with the following Basel requirements:

Capital Adequacy Assessment

Vichara helps its clients to compute capital adequacy reserves needed to comply with various Basel accords.

We enable financial institutions to carry out comprehensive stress tests to capture the effects of credit risk events using both Internal Rating-Based Approach (IRB) as per Internal Capital Adequacy Assessment Process (ICAAP) requirements for Basel II as well as risk weighted assets methodology as required by Basel III.

Stress-testing

Vichara’s solutions help clients perform forward looking risk assessments and measure risk tolerance in adverse scenarios on their portfolios as required by stress tests. Our solutions incorporate macro-economic variables that allow uses to easily define stress scenarios to emulate different types of shocks. The solutions are highly transparent and defendable to withstand any internal or external audit.

IFRS Solutions for Structured Products and Loans

Vichara’s IFRS solutions support both structured products and loan portfolios and ensures full transparency and traceability to satisfy IFRS requirements. Our solutions provide support for:

- Structured Products – RMBS, CMBS, CLOs, CRE CDOs, ABS

- Loans – Residential Mortgages, Commercial Mortgages & Corporate Loans

IFRS 9 – Classification, Measurement & Impairment

To comply with IFRS 9 requirements, Vichara provides:

Impact Assessment & Review

Vichara helps clients determine their readiness to meet IFRS 9 requirements. We review the current processes and credit risk models, map and compare them to IFRS requirements, do a gap analysis and help clients create a road-map to accomplish the required enhancements for IFRS 9.

Impairment Analysis & Expected Loss Modeling

Vichara helps analyze and implement expected loss methodology for timely measurement and recognition of asset impairment to comply with IFRS 9 requirement.

Our solutions integrate with forward looking prepayment, default and loss models for computing expected loss, fair value (using cash flow projections) and impairment recognition (based on stage assignment). The financial assets are categorized according to credit quality (no change, deterioration and impaired) and expected losses (12 month and lifetime) are computed for timely loss recognition as per IFRS 9.

Our solutions can integrate client proprietary models, help clients develop new models or enhance existing models. If clients choose to develop new models or enhance their existing model(s), our modeling framework provides flexibility to incorporate macroeconomic variables (such as GDP, interest rates, unemployment) and asset specific variables (such as HPI, NOI, Cap Rates) as required. The analytics engine provides impairment, credit and cash flow analytics with the ability to generate customized reports as required. Additionally, historical as well as projected analytics are tracked for comparison and audit purposes.